When a company decides to move their business into a new market

and to open up a new office in a new country, one of the first

things to be considered is the country’s tax system. This

article gives further insights on taxation and accounting

requirements in Chile.

Before moving a business into a new market, it is important that

a company fully evaluates these matters to determine if the

company’s existing accounting, finance, and tax professionals

can manage this or if necessary to engage a local professional accounting

services provider for the business. Hence, when making the

decision to move into a new market, the new country’s tax

regime is of high importance and must be taken into

consideration.

Taxation

& Accounting Requirements in Chile

Taxpayers in Chile are companies, individuals and other legal

entities, affecting the income of all corporations and individuals.

Hence, all individuals and companies are subject to an income tax

on their monthly or annual income. Foreign individuals pay income

tax only on their Chilean sourced income during their first three

years in the country, this period can be extended to three more

years, although after that they are also subject to income tax on

their worldwide income.

The tax authority in Chile is the Internal Revenue Service (SII – Servicio de

Impuestos Internos) which is a public organization and depends

on government administration in Santiago, Chile. From the time the

taxpayer filed the return, the tax authority (SII) has an official

three-year time limit in order to review, amend or rectify any tax

return previously filed.

Accounting standards in

Chile

Chile’s accounting

standards are:

Basic financial

statements must include:

- A statement of financial position

- A statement of comprehensive income

- A statement of cash flows

- A statement of changes in shareholder equity

- Notes to the financial statement.

Additionally:

- The presentation currency is the Chilean Peso.

- Concerning accounting laws, all laws registered are defined by

the Codigo

Tributario. - The tax year starts on the 1st of January and ends

on 31st of December in the same year. - Local accounting for companies in a foreign currency (USD, EUR)

is allowed but needs to be specifically authorized and cannot be

changed for (2) years.

Chilean Taxation Number

When carrying out business in Chile a company has to be

registered and obtain a Chilean taxation number and tax ID (RUT).When

a company’s deals with the country’s taxation, this number

is required in order to deal with the national tax authorities.

Moreover, every individual, including foreign individuals in Chile

must obtain a Chilean National Tax ID and a password for the

Chilean IRS website (www.sii.cl)

in order to be able to file their annual tax returns.

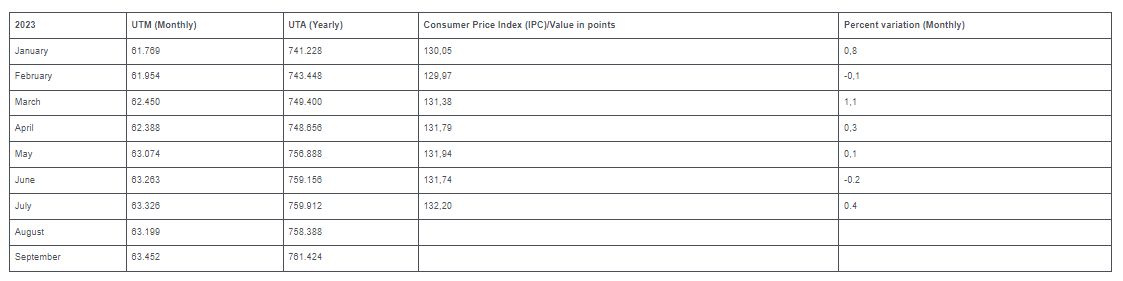

Consumer Price Index (IPC)

In the following table, you can find the values of UTM (Monthly

Tax Unit) and UTA (Yearly Tax Unit) for the months of 2023,

expressed in Chilean pesos (in the first and second columns,

respectively). The remaining columns show the IPC (Consumer Price

Index) for each month of that year and the monthly percentage

variation, accumulated up to the date, and annual variation.

Income Tax

– Accounting Requirements Chile

The Chilean income tax system affects business income, salaries,

other personal income, as well as income which was obtained by

non-residents. Income-tax is structured in different categories and

they have to be applied accordingly. Categories are First Category,

Second Category, Complimentary Global and Additional taxes.

Generally, in Chile two main tax rates have to be taken into

account, the first is the tax rate for companies or corporate tax

(first category

tax), where income is received by exercising commercial,

industrial, agricultural and other activities and the second

important tax is the tax on employment income (second

category tax).

Chile’s

First Category Tax (Corporation Tax)

All companies which are resident and domiciled in Chile are

subject to “First Category Tax” (FCT) and are taxed on

their worldwide income. All company’s non-resident in Chile are

taxed on their income received in Chile only. The first category

tax is calculated on the basis of the company’s taxable profits

generated within a tax year. Additionally, all companies based and

operating in Chile are required by law to make monthly advance

payments (PPM), through monthly declaration (F29), and there is

also a non-obligatory voluntary (PPM) for companies who wish to

keep an additional provision for the yearly income tax, and in the

case of an overpayment the Internal Revenue Service makes a refund

of the exceeded amount.

The first thing the taxpayer must know is the tax regime to

which it is subject, which determines its tax obligations, such as

the filing of certain tax returns.

The taxpayer can consult his current Tax Regime or that of

previous periods in his personal MiSII section by selecting the

option Personal and Tax Data and then Taxpayer Characteristics.

Chile’s Second Category Tax (Personal Income Tax)

The Chilean income tax law is described in detail in the Decree Law 824 of 1974,

known as the Income Tax Law is administered by the Chilean Internal

Revenue Service’s (Servicio de Impuestos Internos). In general,

it can be said that every person working and living in Chile,

resident or nonresident is subject to Chilean income tax. All

entities resident or domiciled in Chile are taxed on their

worldwide income. Non-residents are only taxed on their income

earned in Chile.

Therefore, the Second Category Tax is concerned with all

personal sources of income including salaries, bonuses, gratuities

and other forms of remuneration. The highest progressive rate for

this tax is 40% and all taxes have to be paid on a monthly basis in

accordance with a monthly timetable issued by the Chilean Tax Authority

(Servicio de Impuestos Internos). This tax is deducted from the

gross salary by the employer and subsequently paid over to the

Chilean Internal Revenue Service. Depending on the type of income 6

different income tax rates apply. Furthermore, the income tax is

based on the following two factors:

- The taxpayer’s place of residence

- Source of the income

The taxpayer’s place of residence: In order

to be considered to be a resident, a person has to have lived more

than 6 months within a calendar year in Chile. For non-residents

and non-domiciled the tax rate is 15% if the activities are

technical or professional services if they are not a tax rate of

35% has to be paid on their Chilean-source income alone.

Source of the income: Income is to be

considered Chilean source income, when the income is received while

performing activities within the country, as of services for

businesses and income from property, dividends, royalty and other

income. Therefore, the income is sourced where the service is

provided.

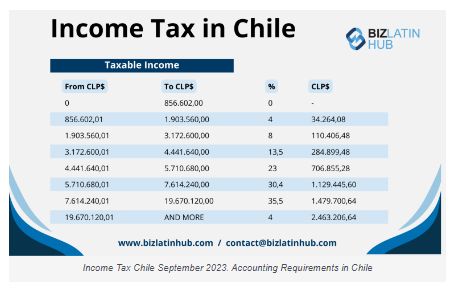

Current Tax Rate in

Chile for 2023

The following table shows the current tax

rate in Chile for September 2023, this table changes on a

monthly basis and income has to be taxed accordingly.

Value-Added Tax (Impuesto al Valor Agregado – IVA) –

Accounting Requirements Chile

Value-added tax in Chile has to be paid on all sales and imports

of goods and services. Furthermore, additional taxes and import

duties have to be applied when importing certain goods such as

beverages, jewels, and others. Currently, the VAT rate is set at

19% of the price of the goods or services. With regards to

importing, the taxable basis is the customs value, CIF Value, which has to be

considered and already includes customs duties. VAT returns must be

filed on a monthly basis.

Regarding exports of goods and services, the VAT rate is zero,

not considering how the product will be exported. Additionally, as

of January 1, 2023 all services (with few exceptions) are taxed

with VAT.

According to the Law, the following services will not pay

VAT:

- Passenger Transportation (Urban, interurban, interprovincial

and rural). - Education (Schools, Kindergartens, Universities, among

others). - Outpatient health services (medical and dental consultations,

psychologists, psychiatrists, kinesiologists, imaging, among

others). - Other services that were already exempted in the VAT Law, such

as: - Tickets to shows (*)

- Lease of unfurnished real estate

- Others (Sales and Services Tax Law Art.12 and 13).

- All other exemptions contained in the VAT Law and other legal

texts remain in force.

Penalties & Fines

When tax returns are not filed within the timetable established

by the tax authorities or if they contain errors, fines have to be

paid. The amount of the fine depends on the length of the debt due

and the channel of payment the taxpayer uses to pay the debt.

Usually, the amount is three times the tax, then the tax initially

due, but when using the SII online payment the percentage of the

fine is lower than when paying at one of the offices directly.

When paying these penalties, the Internal Revenue Service (SII)

has a policy known as (Condonacion) in which if you pay the total

amount of the debt, is up to a discount of 70% of legal fees

(Interest and fines), this a benefit of the new tax reform.

The tax system in Chile is very flexible if everything is always

properly informed, even when in debt; it supports businesses to

keep on growing, through payment facilities.

Other

Employee Contributions – Pension & Health

In general, it can be said that social security deductions make

up to 20% off the monthly salary, these contributions include

payments into the pension fund, the health insurance, unemployment

insurance and the Chilean association of security.

Health Contributions

Chile’s health system has existed since the 1950’s, it

was originally introduced as a national health care system and was

one of the first in Latin America. The relevant agency for the

health care system is the Fondo Nacional de Salud (FONASA). Today

workers can choose between the private health system Instituciones de Salud

Previsional (ISAPRE) and the public health system Fonasa, the

monthly mandatory payment is 7% of monthly income for FONASA and

about 9.2% for the private system ISAPRE.

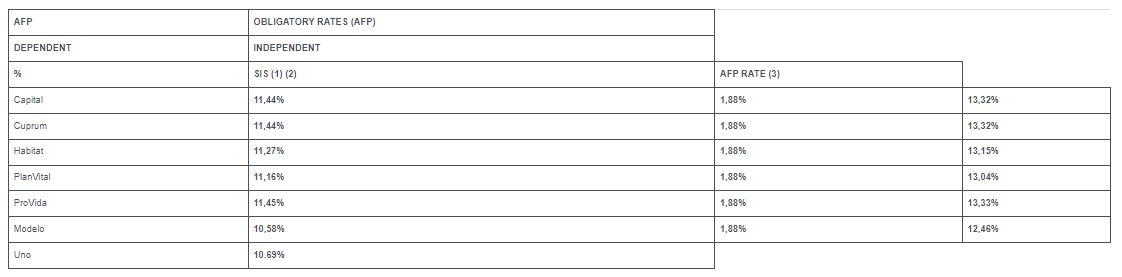

Pension Fund

Contributions

Regarding the pension system, all employees can choose between

six different private pension companies and furthermore are able to

choose between different types of funds. The monthly mandatory

payment on their income is approximately 12%. Any individual can

pay a higher percentage if they decide to. If workers are

self-employed they can decide whether to contribute or not and

which amount they want to contribute on a monthly basis.

(AFP): Pension Fund Contributions

(SIS): Disability and Survival Insurance

1) Employer payment.

2) SIS doesn’t apply for pensioner dependent

employee.

3) This rate includes SIS, which corresponds to the

employee.

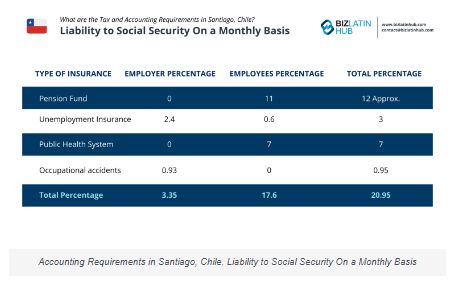

Liability to Social Security On a Monthly Basis:

Common Questions when understanding accounting and taxation in

Chile

Based on our extensive experience these are the common questions

and doubts from our clients when looking to understand accounting

and taxation in Chile.

corporate tax rate in Chile?

In general terms, the rate is 25%. That would be the headline.

Notwithstanding the above, it should be noted that it is constantly

being modified to reduce all the consequences of the pandemic back

to 25%.

taxed in Chile?

In Chile, as far as business is concerned, taxation is based on

income actually received.

Internal Revenue Service (IRS) Called in Chile?

The IRS in Chile is called el Servicio de Impuestos Internos or

in English, The Tax Administration Service, and is responsible for

implementing the fiscal and customs legislation in Chile.

accounting standard in Chile?

Chilean accounting standards require companies to prepare their

financial statements in Spanish and according to Normas

Internacionales de información financiera (NIIF) or in

English IFRS and Principios de la Contabilidad Generalmente

Aceptados. (PCGA)

equivalent in Chile?

The equivalent of a CPA in Chile is aColegio de Contadores

AGcertified public accountant (Contador Publico

Certificado—CPC).

in IFRS?

In general terms, and as far as all BLH clients in Chile are

concerned, according to the current regulations, since 2009 all

companies must follow the IFRS standards.

Biz Latin Hub can help you with Accounting Requirements

Chile

If you want to start a company in Chile, it is advisable that

you have the support of a qualified account and tax specialist from

the start. A well thought out business plan will not be able to

evolve if your business does not remain in good standing with the

local Chilean authorities.

Biz Latin Hub can assist you with all accounting, taxation and

financial matters. Our locally specialist team have a comprehensive

understanding of the local laws and complications in the Chilean

business environment and are well equipped to work with foreign

companies looking to conduct commercial activity in the region.

To learn more about the Chilean economy, the business

opportunities to form a company in Chile, and how you might take

advantage of these politicalshifts, please contact us

today. Or read about our team and

expert authors.

Interested in hiring local staff in

Latin America? See how we can support through either a local

company formation or through a tailored PEO solution.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.