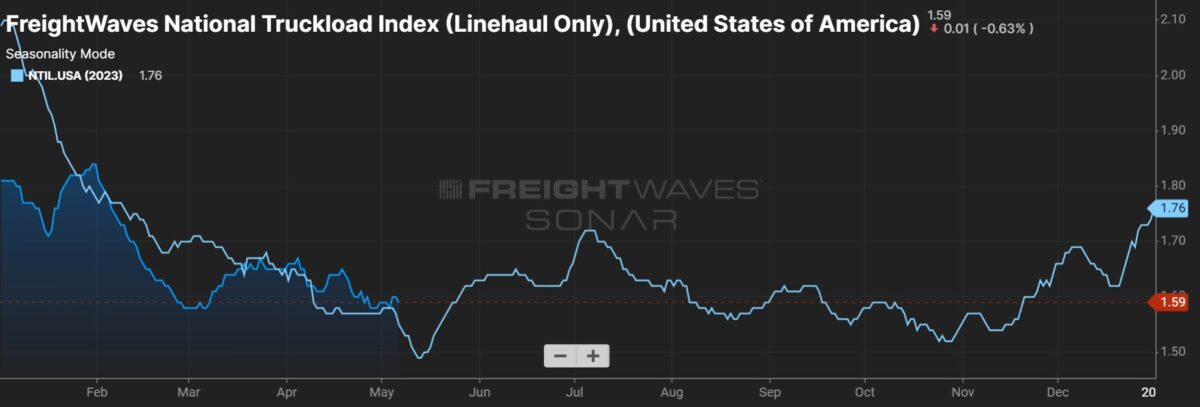

Transportation indicators weakened in April, results of the monthly Supply Chain Sentiment Survey showed on Tuesday. The report highlighted that after three consecutive months of expansion, freight rates have once again fallen into contraction territory.

The transport price sub-index (measured at 44.1) is down 8.9 points from March, with lower fuel prices having a slight impact on the data set. Transport capacity (61.4) increased by 1.8 percentage points and continued to maintain a “solid growth rate”, but utilization rate (56.4) decreased slightly.

The Logistics Manager Index (LMI) is a prevalence index. A reading above 50 indicates expansion, and a reading below 50 indicates contraction.

While a previous report showed “signs that the transportation market is returning towards equilibrium,” the latest update shows it “remains firmly in a freight recession.” The book says:

There was a noticeable downturn in early April, with a 40-point gap between the capacity sub-index and the price data set. But by his last two weeks of the month, prices had risen more than 27 points (into growth territory at 54.8) and production capacity had fallen 10 points to 57.4, so the difference between the two measurements was 3 points. It's now less than

“This could reflect the seasonal restocking of summer items, or the recent Federal Reserve reading may reflect increased expectations that interest rates will fall at the end of the summer. “There is a strong possibility that this is the case,” the report states.

Trucking companies provided another grim update in the first quarter earnings season as overcapacity was slow to clear and rates for some fleets fell below operating costs. However, Schneider National (NYSE:SNDR) pointed to a potential green shoot, revealing that its renewal rate was positive for the first time in six quarters.

“We will need to see several consecutive statistics showing that prices are rising faster than shipping capacity before we can feel confident that the freight recession is over,” the LMI report said. “We are getting closer to late April, but we still have a long way to go before we return to the boom years.”

Respondents expected capacity to increase slowly in the next year (52), while both capacity (68) and prices (73.8) were expected to show strong growth rates. I am.

“Respondents expect the logistics industry to return to boom within the next 12 months,” the report continued. “Whether that happens may depend on whether the trends of late April continue into the remainder of the second quarter.”

The overall LMI reading for April was 52.9, down 5.4 points from March. Although the overall index expanded for the fifth straight month, April's level was the slowest growth rate this year. March's statistics were the highest in 18 months.

Inventory growth has slowed, putting pressure on the index.

Inventory levels (51) fell by 12.8 points during the month, rising from 47.4 in the first half to 53.4 in the second half. The report said the weakness in the first half could be related to expectations that interest rates could remain high, with upstream respondents (manufacturers and wholesalers) readings from March It was noted that it was neutral following 64.8.

“This suggests that manufacturers are holding back on capital until the interest rate picture becomes clearer,” the report said. “A more optimistic April jobs report could have any meaningful impact on this.” I don't know yet whether it will be granted or not.”

It also said the acceleration in inventory levels in the second half may be related to the lingering impact of plans around the Lunar New Year.

Inventory costs (68.5) increased by 1.6 points from March, remaining firmly in expansion mode. In addition to rising interest rates, warehouse prices (63.8) continue to make it more expensive to store goods.

The warehouse price sub-index decreased by 2.5 points during the month as production capacity (54) increased by 9.4 points and utilization rate (55.1) decreased by 8.5 points. The change in warehousing metrics is consistent with logistics real estate operator Prologis' (NYSE:PLD) first-quarter report, which included a slight downgrade to the company's 2024 outlook.

LMI is a collaborative study of Arizona State University, Colorado State University, Florida Atlantic University, Rutgers University, and the University of Nevada, Reno, conducted in collaboration with the Council of Supply Chain Management Professionals.

More FreightWaves articles by Todd Maiden